Buy to Let Mortgages

How does a Buy to Let mortgage work?

Over the last 17 years I’ve seen the Buy to Let mortgage market change a lot, but the basics have remained the same.

Many of my clients have become landlords through wanting to keep their current home and using it to fund an onward purchase, or remortgaging to buy an investment property. Whatever reason you have you still need to understand the tax implications of owning a second property.

As the property will be generating an income you’ll be required to complete a tax return each year, which if you are employed will be a new experience. Our advice before going into any Buy to Let mortgage is to seek Independent Tax and Accountancy Advice as there are many costs to consider and it’s worth finding out if the property will be making, or costing you money.

There’s a helpful guide to many aspects of Buy to Let ownership in the Blog section.

Unlike a residential mortgage where the lender is purely focused on your income and outgoings the Buy to Let mortgage lender needs some basic requirements to be met before lending any money. Therefore, you must be able to show that you;

As always, the above is only a guide as mortgage lenders can differ, but if you want to Buy to Let, get in touch with me to discuss your individual circumstances and I’m sure we’ll find a solution.

Example of a Buy to Let Mortgage

Let’s take a very simple purchase of £200,000.

You’ll need a 25% deposit of £50,000 which leaves a mortgage requirement of £150,000. It’s the rental figure the property will generate per month that will decide whether you can borrow that £150,000.

Now, there are many rental assessments out there but let’s use an example.

Take the rent of £750 per month, multiply it by 12 and divide by 145%. Divide again by 5%. This would give you a loan size of £124,137. As you can see this is far less than required so you would have to increase your deposit to £75,863.

But if the rent was £1,000 per month and we used the same calculations you would get a loan of £165,517. You now need to remember that the maximum the lender will offer is 75% so although the rental income will generate more, it’s irrelevant, with maximum lending kicking in at £150,000.

Buy to Let Personally vs Limited Company (Ltd)

Once again I would suggest speaking with an accountant about the tax position of each structure as it can make a big difference to the profitability of the ownership. MK Mortgages can help with this by providing two sets of data to show the difference between the mortgage rates that will be offered.

As a general rule of thumb, the Ltd. company mortgage rates are higher and come with higher set up fees, plus require personal guarantees to be given, again another cost.

I have some guidance notes on the differences and benefits between the two options, but when setting up a company to purchase a Buy to Let property, it needs to be a Special Purpose Vehicle (SPV). The company will also need a specific Standard Industrial Classification code (SIC). These ideally needs to be one of the three from the below list.

I could easily fill several pages with information on Buy to Let mortgages, so if you’ve read enough and want to know more about your own choices, please get in touch.

! Please note, some Buy to Let mortgages are not regulated by the Financial Conduct Authority.

What we do

I pride myself on being up to date with regulation, legislation and the economic market. I work to understand your needs, match that to the requirements of lenders, and protect you and your dependants once you have bought your property.

This way, I can help you save time and money in the new world of mortgage advice.

The no-nonsense approach to mortgage advice

Contact MK Mortgages

Please use the contact form to get in touch. The earlier you start the process the better.

Marc Kavanagh is a non-fee charging, whole of market mortgage adviser, providing advice purely for your benefit.

I cannot recommend Marc and his team highly enough. They helped and supported me throughout the whole process of buying my first home and were always kind and professional.

Marc and Sooz made everything as simple as possible and went above and beyond to help. They were always there for guidance and to answer any questions, which was amazing as I was embarking on a process I had very limited knowledge about. I’m not sure I would have been able to do it without them!

E Brooks

Fantastic experience – Marc and Sooz have been outstanding from start to finish in helping guide me through the complex process of finding a suitable mortgage for a first-time buyer. Marc even helped guide me on what best/worst attributes to look out for when house hunting, and what kind of offers should be pitched to the vendors in the current market.

Other additional services such as mortgage cover were offered, but never pushed – which I appreciated.

Very easy to deal with and get in contact with when needed, professional at all times – Highly recommend MK Mortgages.

C Richards

What paperwork is needed to apply for a mortgage?

You want to apply for a mortgage, but do you know what paperwork is needed to get started? As trusted mortgage advisers we have a requirement to fully understand our

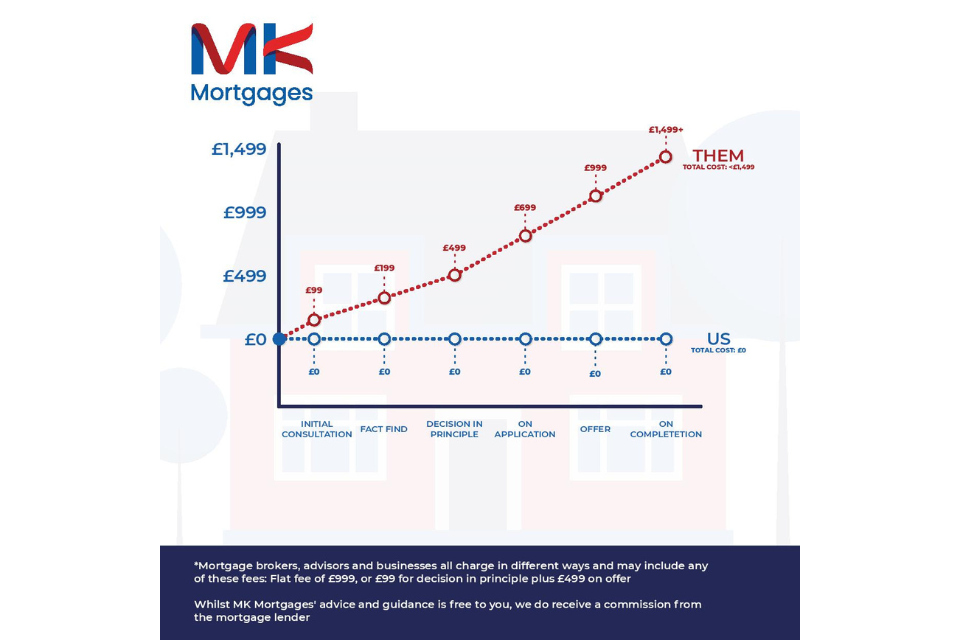

No-fee mortgage advice – But HOW can we do that?

Most people would see that something is free, and think to themselves, ‘what’s the catch?’. And to be fair, you’d be right to assume that it could mean hidden charges,